Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Ireland

Ireland

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

Ireland

India

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Kingdom

United Kingdom

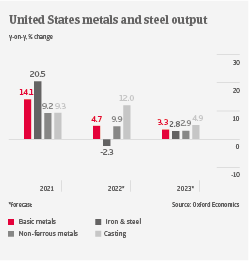

United States

United States

After a very high growth rate in 2021, US metals and steel output is expected to increase by about 5% this year, driven by ongoing robust demand, mainly from residential construction, aerospace, transportation and engineering. However, the decrease in automotive sales in H1 of 2022 indicates diminishing demand for high priced, metal-intensive consumer products, given high fuel costs and consumer price inflation. Order backlogs persist amid supply chain constraints. While oil and gas prices have sharply increased, the robust demand enables metals and steel businesses to pass on higher input prices. The industry benefits from the fact that some US manufacturers have moved production back home in order to avoid further supply chain disruptions and to improve price stability.

That said, the US metals and steel industry is facing increased competition from EU peers in its domestic market, due to the partial scaling back of Section 232 tariffs for EU imports and the weaker EUR compared to the USD. This will cap domestic production growth in 2023, when we expect production to increase by about 3%.

Persistent high inflation remains a downside risk, as it could trigger more aggressive monetary tightening by the Federal Reserve. A hard economic landing would result in decreasing consumption and investment, dampening metals and steel demand. In such a scenario, we would expect metals and steel output to contract by about 1% in 2023.

Payment duration in the metals and steel sector has improved to 45 days on average in 2022, compared to 81 days in 2021, because most buyers could not demand longer payment terms in a market environment of high demand coupled with supply issues. However, a majority of businesses anticipate longer payment terms to return in the mid-term. The amount of non-payments and insolvencies has been low in 2021 and H1 of 2022, and we expect no deterioration in the coming twelve months. While metals and steel businesses are highly dependent on bank financing, gearing of businesses is generally stable. Banks are willing to provide loans to capital-intensive metals and steel businesses that are consistently profitable. Our underwriting stance remains neutral across all main subsectors (iron and steel, non-ferrous metals, casting and metals manufacturing).